Certificate of Deposit

A negotiable certificate of deposit, or NCD, is a large certificate of deposit that is typically purchased by institutional investors.

Often called a Jumbo CD, an NCD is frequently a suitable investment for an institution or company that has a large amount of money it will not need to use for several weeks or months. Prior to the debut of NCDs, banks could not compete for such investments because they could not offer a rate that compared to those from other money market instruments.

An NCD is a low-risk, low-interest deposit that is loaned to a bank for certain period of time. NCDs have a minimum face value of $100,000, but they are typically $1 million or more.

Unlike a regular CD, NCDs pay periodic interest, usually twice a year. The bank that issues the NCD guarantees it, and redeems it at face value plus interest at maturity. NCDs cannot be cashed in before reaching maturity, but can be easily sold in the open market before that time.

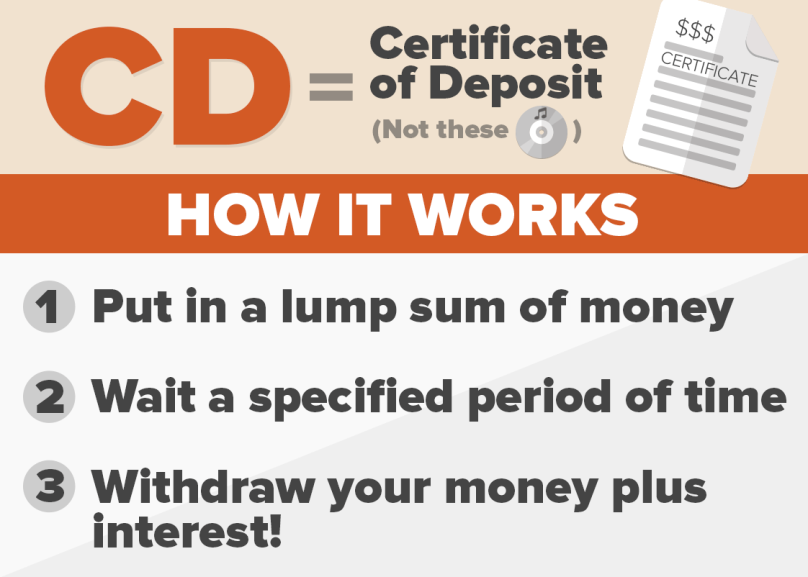

Certificate of Deposit

A certificate of deposit (CD), is a common financial product sold by banks, thrift organizations and credit unions. Customers buy CDs to earn interest while keeping their money safe. Bank CDs are insured up to $250,000 in the U.S by the Federal Deposit Insurance Corporation (FDIC) and are usually considered risk free.

Because they are virtually no-risk, their interest rate is among the lowest of any financial product. Financial products that involve more risk and are not insured by the FDIC or any other entity tend to pay higher interest rates.

To buy a CD, customers agree to deposit their money for a specified period of time. The shortest timeframe is usually one month, with the longest running up to five years.

In return for committing their money for a period of time, the customer earns interest. The interest rates are pre-determined by the institution, and typically remain fixed over the length of the CD – though some institutions may offer CDs whose rates can increase. The longer the length of the CD, typically the higher the interest rate paid.

When the CD’s time period is complete, a CD is said to “mature.” Shortly before this, the institution will notify the customer, offering them the option to either withdraw the money with interest earned, or re-invest the money for another period.

CDs pay slightly higher rates than savings and checking accounts because the customer commits to not withdrawing their money for a specified period of time – whereas money in savings and checking accounts is able to be withdrawn at any time. If they need to, customers may withdraw their money before the CD matures. However, this requires a penalty to be paid.

CDs typically range in size from $1000 to over $100,000. Larger CDs over $100,000 are typically called Jumbo CDs.